A sole proprietorship, also known as a sole trader-ship, individual entrepreneurship or proprietorship, is a business that can be owned and controlled by an individual or person in which there is no legal distinction between person and legal entity

Benefits to registered your business as of Sole Proprietorship.

Single Ownership: A sole proprietorship is owned and operated by a single individual. This individual makes all decisions regarding the business and retains all profits.

Ease of Formation: Establishing a sole proprietorship is relatively easy and inexpensive compared to other forms of business entities. There are minimal legal formalities involved in setting up a sole proprietorship.

Direct Control: The owner has complete control and authority over all aspects of the business, including decision-making, management, and operations. This allows for quick decision-making and flexibility in adapting to changes.

Sole Responsibility: The owner bears sole responsibility for the liabilities and debts of the business. Personal assets are at risk in case of business losses or legal claims, as there is no legal separation between the owner’s personal and business assets.

Taxation: Income from the sole proprietorship is typically taxed as personal income of the owner. The business itself does not pay separate income taxes. The owner reports business income and expenses on their personal tax return.

Minimal Regulatory Compliance: Sole proprietorship are subject to fewer regulatory requirements compared to other business structures such as corporations. There is no need for formal registration with the government unless the business operates under a trade name different from the owner’s name.

Flexibility: Sole proprietorships offer flexibility in terms of management and decision-making. The owner can quickly adapt to market changes, pursue new opportunities, or make changes to business operations without the need for extensive consultations or approvals.

Limited Resources: Sole proprietorships may have limited access to capital and resources compared to larger businesses or corporations. This can constrain growth opportunities and expansion plans.

Limited Life Span: The life span of a sole proprietorship is tied to the life of the owner. In the event of the owner’s death or decision to cease operations, the business typically ceases to exist unless it is transferred or sold to another party.

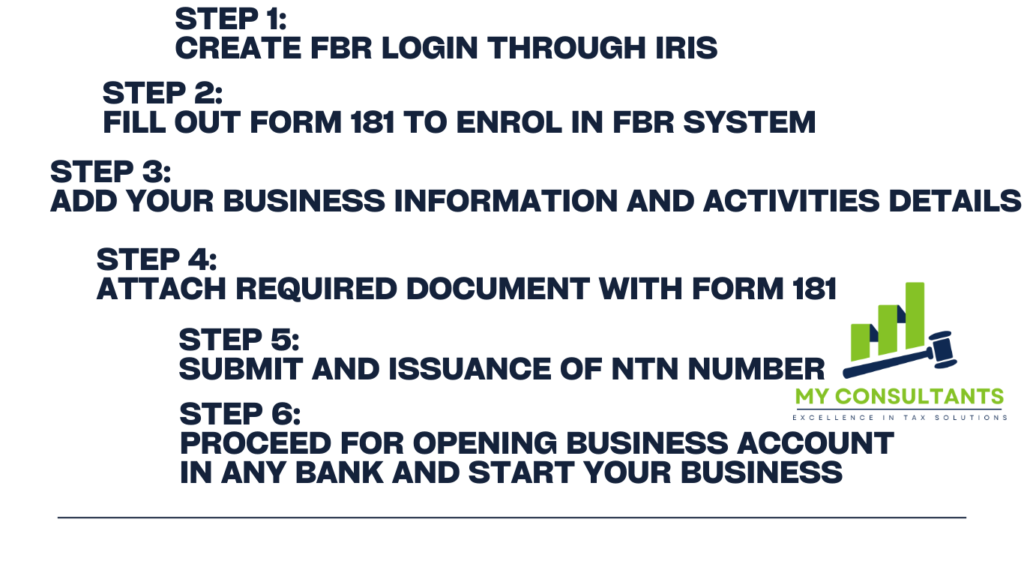

Steps to get registration of business as sole proprietorship in Pakistan

[…] of sale tax, it is important that the person already registered his business in the form of Sole Proprietorship, Single Member Company, Association of Partnership, Private Limited Company or Public Limited […]

3 comments

[…] of sale tax, it is important that the person already registered his business in the form of Sole Proprietorship, Single Member Company, Association of Partnership, Private Limited Company or Public Limited […]

[…] In an unregistered business, especially for sole proprietorship’s, the owner is personally liable for all business debts and legal […]

Your article helped me a lot, is there any more related content? Thanks!